Benjamin Graham Intrinsic Value Formula Explained

TL;DR:

- The Benjamin Graham intrinsic value formula estimates a company’s fair value using earnings, growth, and bond yields. It is best suited for stable companies and serves as an initial screening tool. Applying a margin of safety and combining it with other valuation methods improves investment decisions.

The Benjamin Graham intrinsic value formula is defined as V = [EPS × (8.5 + 2g) × 4.4] / Y, where EPS is trailing twelve-month earnings per share, g is the expected 7–10 year earnings growth rate, and Y is the current AAA corporate bond yield. Originally published in 1962 and revised in 1974 to include a bond yield adjustment, this formula gives investors a fast, disciplined estimate of what a stable stock is worth. It sits at the core of Graham value investing and works best as a screening tool, not a final verdict. Understanding how to calculate intrinsic value with this method, and when not to, separates investors who use it well from those who misapply it.

How to calculate intrinsic value using the Benjamin Graham formula

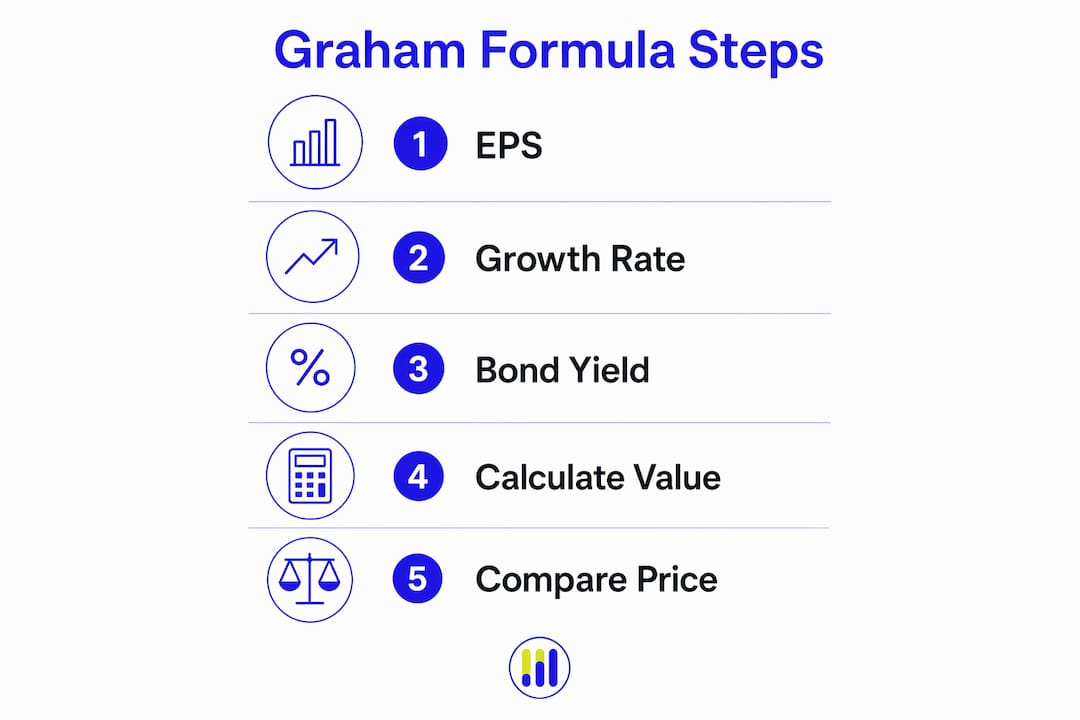

The revised Graham formula V = [EPS × (8.5 + 2g) × 4.4] / Y requires three inputs. Each one affects the output significantly, so accuracy at this stage matters more than speed.

Step 1: Find trailing twelve-month EPS. Pull this figure from the company’s income statement or any major financial data provider. Use diluted EPS for a more conservative result.

Step 2: Estimate the growth rate (g). This is the projected annual earnings growth rate over the next 7–10 years. Conservative growth estimates yield more reliable valuations. For a mature consumer staples company, a g of 5%–7% is reasonable. For a utility, 3%–5% is more appropriate.

Step 3: Find the current AAA corporate bond yield (Y). As of march 2026, the AAA corporate bond yield was approximately 5.2%. This figure changes over time, so always use a current source.

Step 4: Plug in the values. Take a hypothetical company with EPS of $4.00 and an estimated growth rate of 6%. Using Y = 5.2%:

V = [$4.00 × (8.5 + 12) × 4.4] / 5.2 V = [$4.00 × 20.5 × 4.4] / 5.2 V = $361.20 / 5.2 V ≈ $69.46

Step 5: Compare to the current stock price. If the stock trades at $50, it appears undervalued. If it trades at $85, the formula suggests overvaluation.

Pro Tip: Use a growth rate at the lower end of analyst estimates. Overestimating g inflates intrinsic value and creates a false sense of safety.

What are the limitations and suitable uses of Graham’s formula?

The Graham formula is a quick screening tool, not a full business appraisal. Knowing where it works and where it breaks down is what separates disciplined investors from those chasing numbers.

The formula works best for:

- Stable, established companies with predictable earnings, such as utilities, consumer staples, and mature industrials.

- Companies with consistent EPS growth over at least five years, where a 7–10 year projection is grounded in history.

- Initial screening to flag stocks worth deeper research, not as a buy or sell trigger on its own.

The formula is less reliable for:

- Early-stage or high-growth companies where earnings are negative or highly variable.

- Cyclical stocks in industries like mining or airlines, where EPS swings wildly across economic cycles.

- Financial companies where book value and regulatory capital matter more than earnings growth.

Failing to update the bond yield Y inflates or deflates intrinsic value improperly. A stale Y from a low-rate environment will produce an unrealistically high valuation in a higher-rate market. Applying the formula alongside DCF models, P/E multiples, and qualitative analysis leads to better-informed decisions.

Pro Tip: Never use the formula output alone to make a buy decision. Treat it as a first filter, then conduct full fundamental research before committing capital.

How does the Graham formula differ from the Graham Number?

Investors frequently confuse the Graham formula with the Graham Number. The two serve different purposes and target different investor types.

The Graham Number is calculated as: Graham Number = √(22.5 × EPS × Book Value per Share). It acts as a price ceiling for defensive investors. A stock trading below its Graham Number is considered conservatively priced relative to both earnings and assets.

The intrinsic value formula, by contrast, incorporates expected growth. It rewards companies with strong earnings trajectories, making it more suitable for growth-oriented value investors.

| Feature | Intrinsic value formula | Graham Number |

|---|---|---|

| Inputs | EPS, growth rate, bond yield | EPS, book value per share |

| Purpose | Estimate fair value with growth | Set a defensive price ceiling |

| Best for | Stable growth companies | Asset-heavy, defensive stocks |

| Interest rate sensitivity | Yes, via Y adjustment | No |

| Investor type | Growth-aware value investors | Defensive, conservative investors |

Using both formulas together gives you a fuller picture. If a stock passes the intrinsic value formula screen and also trades below its Graham Number, the margin of safety case becomes considerably stronger.

How can individual investors apply the Graham formula in their workflow?

The formula works best as the first step in a structured research process, not a standalone answer. Here is how to integrate it effectively:

- Screen for candidates. Use the formula to identify stocks where the calculated intrinsic value exceeds the current price by at least 20%–30%. A 20%–30% margin of safety is standard among value investors and protects against estimation errors.

- Check EPS quality. Confirm that earnings are real and recurring. Exclude one-time gains or write-downs from your EPS figure before applying the formula.

- Validate the growth rate. Cross-reference your g estimate with analyst consensus, historical earnings growth, and industry trends. A growth rate that looks optimistic on paper often collapses under scrutiny.

- Run complementary valuation methods. Use alongside DCF models, P/E multiples, and qualitative analysis to triangulate a fair value range rather than relying on a single number.

- Assess qualitative factors. Industry stability, management track record, competitive position, and balance sheet strength all affect whether a company can sustain the growth rate you assumed.

- Update your inputs regularly. Bond yields shift with monetary policy. A valuation built on a 3% yield looks very different at 5.2%. Recalculate whenever macro conditions change materially.

Tickerplace offers an intrinsic value calculator that applies Graham’s method alongside other valuation models, making it straightforward to run this analysis without building a spreadsheet from scratch. For investors who want to screen across thousands of stocks, the Tickerplace stock screener lets you filter by valuation metrics to surface candidates worth investigating further.

Key Takeaways

The Benjamin Graham intrinsic value formula is a disciplined screening tool that estimates fair value using earnings, growth, and bond yields, and works best when applied with a margin of safety and complementary valuation methods.

| Point | Details |

|---|---|

| Formula definition | V = [EPS × (8.5 + 2g) × 4.4] / Y; always use current AAA bond yield for Y. |

| Best use case | Stable, established companies with predictable earnings; not suitable for early-stage or cyclical stocks. |

| Graham Number distinction | The Graham Number uses book value as a price ceiling; the intrinsic value formula incorporates growth expectations. |

| Margin of safety | Apply a 20%–30% discount to the formula output before treating a stock as undervalued. |

| Workflow integration | Combine with DCF analysis, P/E multiples, and qualitative research for well-rounded investment decisions. |

The formula is a compass, not a GPS

At Tickerplace, we have run Graham’s intrinsic value calculation across thousands of stocks, and the pattern is consistent: the formula is most valuable when investors treat it as a sanity check rather than a verdict. The number it produces is only as good as the growth rate you feed it. Optimistic growth assumptions are the single most common way investors misuse this method, and the resulting overvaluation can look perfectly reasonable on paper until earnings disappoint.

The bond yield adjustment is the part most investors ignore, and it matters enormously. A valuation built on a 2% yield in 2021 would produce an intrinsic value roughly 2.5 times higher than the same calculation run at 5.2% in 2026. That gap is not a rounding error. It is the difference between a stock appearing deeply undervalued and appearing fairly priced.

The formula’s real strength is discipline. It forces you to quantify your growth assumptions and confront the opportunity cost of capital. Pair it with a genuine margin of safety, cross-check it against a DCF model, and use it to narrow your research list rather than close it. That is how Graham intended it to work, and that is where it still delivers value today.

— Tickerplace

Stock valuation tools for individual investors

Tickerplace gives individual investors free access to institutional-grade valuation tools, including a dedicated stock valuation calculator that applies Graham’s formula alongside P/E and P/S models. Every calculation pulls current EPS data and lets you adjust the growth rate and bond yield manually, so your intrinsic value estimate always reflects current market conditions.

The stock valuation checker goes further, running multi-model valuation across thousands of US and ASX-listed equities and flagging whether each stock appears overvalued or undervalued right now. No spreadsheets, no manual data entry. Tickerplace updates valuations daily so your analysis stays current without extra effort on your part.

FAQ

What is the Benjamin Graham intrinsic value formula?

The Benjamin Graham intrinsic value formula is V = [EPS × (8.5 + 2g) × 4.4] / Y, where EPS is earnings per share, g is the expected growth rate, and Y is the current AAA corporate bond yield. It estimates the fair value of a stable, profitable company.

How does the bond yield affect the Graham formula?

The bond yield Y acts as a discount factor. A higher Y reduces the calculated intrinsic value, reflecting the higher opportunity cost of capital in a rising-rate environment. Using an outdated Y produces misleading valuations.

What is the difference between the Graham formula and the Graham Number?

The Graham formula estimates intrinsic value using earnings and growth; the Graham Number uses earnings and book value to set a defensive price ceiling. The two tools target different investor goals and should not be used interchangeably.

What margin of safety should I apply to the Graham formula output?

A 20%–30% margin of safety is standard among value investors. This means only considering a stock undervalued if its current price is at least 20%–30% below the calculated intrinsic value.

Is the Graham formula suitable for all stocks?

The formula works best for stable companies with predictable earnings, such as utilities and consumer staples. It is not reliable for early-stage companies, cyclical stocks, or businesses with negative or highly volatile earnings.